You bought a newly launched Condo about 3-4 years back and the Condo has now reached TOP (Temporary Occupation Permit) status. This is cause for celebration since your long-awaited condominium is now ready for move-in. But you realize that the monthly installment is also much higher now because of the additional drawdown on your loan upon TOP, as well as the surge in interest rates (due to the 11 interest rate hikes since March 2022 by the US Federal Reserve).

Back in 2020, the interest rate for home loans was close to 1%. At the time of this article, homeowners who are on Floating Rates are paying 4-5% interest rates after their lock-in period expired because the common Reference Rates that most home loans are pegged to such as 3-month SIBOR or 3-month SORA, are now at all time high of 4.05% and 3.70%, before factoring in the typical Loan Spread of 0.75%-1.00%. Hence, the effective interest would be 4.50%-5.0%.

The savvy homeowners will consider refinancing their loans. However, some of them might have the misconception that they cannot refinance before the property’s Certification of Completion (CSC) – usually 12 months after TOP. The reason is that before the property reaches CSC, there will still be 15% of the loan which is undisbursed by the current bank, according to the normal Progressive Payment Schedule.

So, can you Refinance before the CSC?

Yes – you definitely can! However, there is a penalty for redeeming the loan before the CSC known as the Cancellation Fee. Depending on your Letter of Offer, the penalty could amount to 0.75% of the undisbursed loan amount. You will need to work out the savings (by Refinancing) and compare it to the Cancellation Fee and other costs involved to see whether it makes sense.

Here’s a quick example of one of our recent refinancing case involving a project that just TOP:

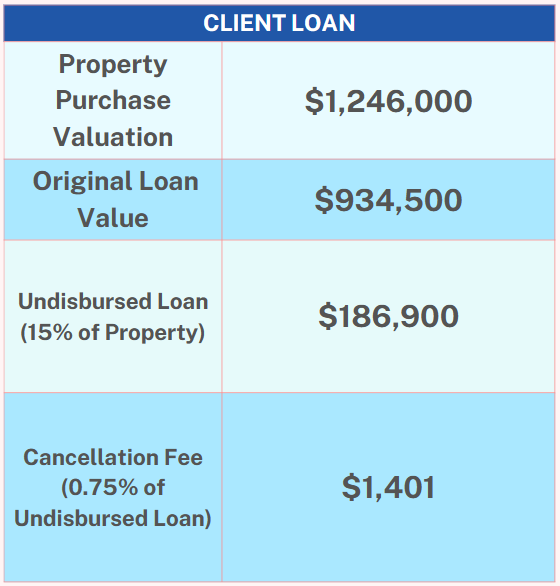

The property was purchased for $1,246,000 in April 2021, so the original Loan amount is $934,500 over a 24 year period, and the interest rate is pegged to the bank’s internal mortgage board rates + loan spread of 0.3% for the first 3 years. The loan spread will then increase from +0.3%, to +0.8% in year 4, and +1% in year 5.

While interest rates were low initially (around 1% for year 2021), it started surging aggressively due to the 11 rounds of interest rate hikes by the US Federal Reserve as mentioned above.

When the client came to us, the outstanding loan was around $910,000, with an interest of 3.9%. In April 2024, it will rise to 4.4% (Year 4 of loan), and she will be paying $5538.95 per month.

To help this client lower her interest rates, we helped her to compare packages from various banks and eventually secured a 2-year fixed rate package of 3.05%. She also received a cash rebate from the new bank, which can be used to cover her legal fee and valuation fee.

However, recall that there is still an undisbursed loan amount of 15% of purchase price, which equates to $186,900. Based on her original letter of offer, the cancellation fee is 0.75% of the undisbursed loan amount. Hence the cancellation fee amounts to $1,401.

By Refinancing her loan, she will save around $12,182 in interest in just the first year alone. Over 2 years, the interest savings will be $25,879. Even after factoring in the Cancellation Fee, she will still save $24,478 over two years! Think about what you can do with this $24K of extra cash!!

Many homeowners make the mistake of thinking that they are unable to refinance their loans before the Certification of Statutory Completion,

Or are worried about the perceived high costs of Cancellation Fee. However, once you break down the numbers, you quickly realize that long-term savings far outweigh any short-term losses. Especially right after the Condo reaches TOP status.

If you are wondering whether you are eligible to save on your home loan interest, you can connect with one of our mortgage experts who can help you do a complimentary assessment of your situation. You can contact us via the links below: