In “The 7 Habits of Highly Effective People,” one habit distinguishes effective people from average ones: begin with the end in mind. Successful people are goal-oriented, and they are clear about their end goals BEFORE they even get started.

Successful property investors also begin with their end goal (exit strategy) before making their purchase, which means they think two steps ahead even before taking out their cheques. Successful investors think about their exit strategy (Who will be the next buyer, What kind of price they can reasonably sell at, When to sell, etc) before they even make the purchase – begin with the end in mind! This does not mean that what they think will necessarily come true. However, this process of thinking ahead can help them identify certain problems and pre-empt them. And in event they feel that the chances of them being able to exit with their predetermined conditions are low – they may not even proceed with the purchase.

Average investors, on the other hand, think only about the first step – Buying. Because of Fear Of Missing Out (FOMO), they rush to buy a new launch because of the fear that the project might sell-out soon. When they arrive at the fashionably-designed showflat and are treated to a warm welcome by the property agents on duty with a cappuccino and sometimes complimentary snacks served, they get completely overwhelmed and “sold”. What’s needed to complete the purchase is just for the agent to ask “So, Mr XX, which unit do you prefer – “10-03” or “12-08”?” And the Deal is done! So, avoid making decisions inside the showflat at all cost!

Let’s run through a hypothetical scenario in a successful property investor’s shoes.

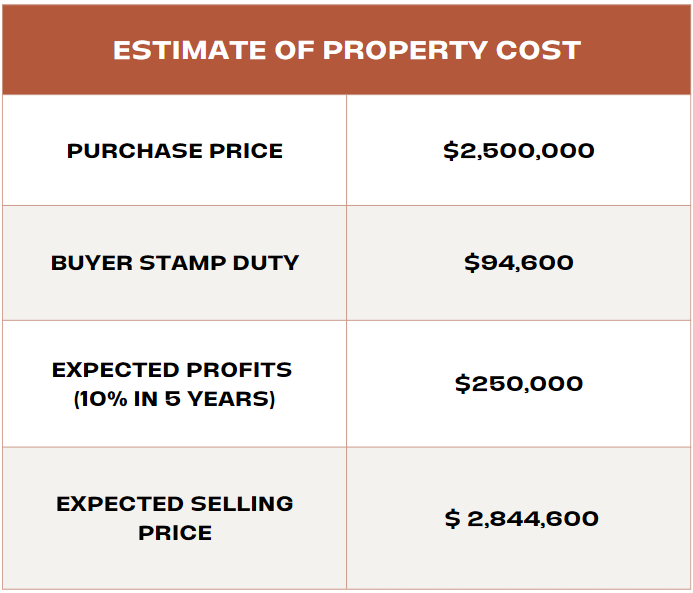

A new Private Condo project launches, selling quickly due to its amazing amenities and potential for future growth. A 1,000 square foot unit costs $2,500 per square foot, totaling $2,500,000 per unit. Including buyer stamp duty of $94,600, the total cost is $2,594,600.

Now, here is where the successful investor will think 2 steps ahead and take it a step further than the average investor. He would think about the scenario and conditions when he needs to sell in say 5 years’ time.

Let’s say he plans to sell in 5 years, aiming for a 10% profit, or $250,000. This means selling the unit for $2,844,600, which is inclusive of the 10% profit and the buyer stamp duty paid during the initial purchase.

The question this Successful Investor will ask is – how feasible is it to sell at $2,844,600 in 5 years’ time?

Thinking from the future buyer’s shoes.

Now that the investor has an estimate of the price he plans to sell the unit after factoring in his profit target (for taking the risk), he will now have to assess who his buyer is likely to be, and what would be going through the future buyer’s mind.

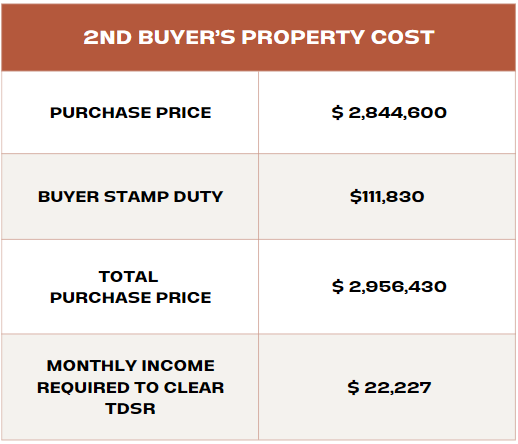

To afford the property at $2,844,600, the next buyer faces a stamp duty of $111,830, bringing the total costs to $2,956,430. Let’s look at the mortgage and its income requirements next.

The required mortgage loan would be $2,133,450 (assuming a Loan to Valuation of 75%). Assuming the Medium Term Interest Rate used by banks at 4.8% and a 25 year loan, the monthly installment works out to be $12,176. To fulfill the TDSR (55%) requirements, the next buyer needs to have a monthly income of $22,227 at minimum, assuming he has no other existing debts such as car loans or personal loans.

The next buyer needs to be earning at least $22,227 monthly, have $822,980 for upfront payment ($711,150 for downpayment and$111,830 for buyer stamp duty), and in order to qualify for a 25 year loan with 75% LTV, he cannot be older than 40 years old.

So, WHO fits into such a profile?

This person is possibly a senior director in an MNC to command such a high pay, and likely with a family. As such, a 1,000 sq. ft. unit might not be able to accommodate his family needs. Hence, he is unlikely to be a potential buyer due to the size as he would likely require a bigger house for his family.

Through this analysis, the investor sees that the assumptions he made may not be possible. And while the property might appreciate, it may be beyond the reach of his next buyer or it would be extremely difficult to sell. From here, he needs to decide whether it still makes sense to proceed with the purchase.

It is not uncommon to hear about people losing money on property despite the Singapore property market having a good run for the past 15 years. However, by thinking two steps ahead and profiling future potential buyers, Successful Investors can better assess a property’s viability and weigh the pros and cons of going ahead.

When purchasing a property, it is prudent for buyers to think two steps ahead. How much profits can they reasonably expect? Who will be able to buy at that price? Does the property appeal to that profile of buyer? By asking these questions, buyers can then better assess how profitable their property can be. And how feasible it is to find a future buyer at their expected selling price say 5 years down the road.

When you decide to purchase a property, you will also need access to the most suitable loan package. You can reach out to our mortgage experts for a free consultation via the link in the description below: