Up to 37% of your cumulative gross income from your working years is sitting in your Central Provident Fund (CPF) account, waiting to support your future needs. That’s a significant chunk of your money, and ensuring it ends up with your intended beneficiaries when you’re no longer around is crucial.

Despite that, few truly understand what CPF Nomination entails and why it’s important. Whether you’re planning for the future or just curious, it’s crucial to grasp how CPF nomination works and how they can impact your loved ones in the future.

What Is a CPF Nomination and Why Does It Matter?

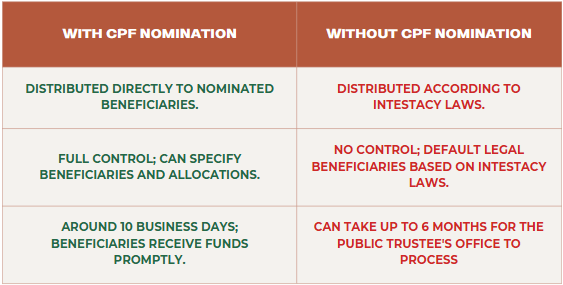

A CPF nomination is a formal declaration that dictates how your CPF savings will be distributed upon your death. Essentially, it allows you to specify who should receive your CPF savings and in what proportion. Without a CPF nomination, your savings will be distributed according to the laws of intestacy, which may not align with your personal wishes. This process can ensure that your CPF savings are given to the right people or entities, providing financial support to those you care about or causes you believe in.

It is also important to note that CPF Nomination covers only the following:

- CPF savings* in your Ordinary, Special, MediSave, and Retirement Accounts

- CPF LIFE unused premiums

- Discounted Singtel shares

CPF Nomination does not cover:

- Properties bought using your CPF savings

- Payout from Dependants’ Protection Scheme (DPS)

- Investments made under CPF Investment Scheme

Let’s dive into the 6 things you may not know about CPF Nominations:

- Wills Cannot Be Used for CPF Funds Distribution

One common misconception is that a will can cover all aspects of your estate, including CPF savings. However, this isn’t the case. CPF savings are not considered part of your estate. This means that they cannot be included in your will for distribution. Instead, you must make a CPF nomination to ensure that your CPF savings are distributed according to your wishes. This arrangement protects your CPF savings from creditor claims on any outstanding debts you may have, and preserves your savings fully for your nominees or family members.

- Marriage Will Revoke Any Existing Nominations

Marriage is a significant life event that can affect many aspects of your financial planning, including CPF nomination. When you get married or remarried, any existing CPF nomination you have made will be automatically revoked. This means you will need to make a new CPF nomination to reflect your current circumstances and ensure that your CPF savings are distributed as you intend. It’s important to remember this automatic revocation to avoid unintended consequences, such as your savings being distributed according to intestacy laws rather than your preferences (e.g. your parents).

Consider the story of a young couple, newly married, full of hope for the future. They’re busy planning their life together but overlooked updating their CPF nominations. If one of them were to pass away, the funds might go to unintended beneficiaries like parents or siblings instead of the surviving spouse.

- Divorce Does Not Revoke Existing Nominations

Unlike marriage, divorce does not automatically revoke existing CPF nominations. This means that if you get divorced and you had previously nominated your ex-spouse as a beneficiary, he will still be entitled to receive your CPF savings unless you had updated your nomination. It’s crucial to review and update your CPF nomination after a divorce to ensure they align with your current wishes.

Imagine going through the emotional turmoil of a divorce only to realize later that your ex-spouse is still entitled to your CPF savings because you didn’t update your nomination. This oversight could lead to unnecessary complications and distress for your loved ones, in event of your passing.

- You Can Nominate Charities or Entities as Nominees, But You Must Go to the CPF Office

You have the flexibility to nominate anyone as a beneficiary of your CPF savings, including charities or other entities. However, if you wish to nominate a charity or an organization, you must do so in person at a CPF service centre. This additional step is required to ensure the nomination is handled correctly and that your charitable intentions are clear and legally binding. This process ensures that your CPF savings can support the causes you care about, leaving a legacy that reflects your values and priorities.

- Nominations Can Be Done Online on the CPF Website

For individual nomination, the process is straightforward and can be conveniently completed online. The CPF website provides a user-friendly platform where you can make, update, or revoke your CPF nomination from the comfort of your home. This online service simplifies the process, making it accessible and easy to manage. By leveraging the online nomination system, you can ensure that your CPF savings are directed according to your current wishes, without the need for paperwork or physical visit to the CPF Board.

Think about the convenience of being able to manage your CPF nomination from the comfort of your living room. It’s a seamless way to ensure your financial legacy is in order, adapting easily to changes in your life circumstances. Basically, there is no excuse for not making your nomination now that it’s made so convenient.

- The 99%-1% Allocation

When nominating your wife as your primary beneficiary and you have children, consider the strategic allocation of 99% to your wife and 1% to your children. This thoughtful distribution plan serves a dual purpose: if both you and your wife pass away, the CPF funds will automatically pass down to your children, bypassing the intestacy laws. This not only eliminates the administrative fees that the Public Trustee will be charging if there is no nomination done, but also ensures a faster transfer of funds.

Contrast this with the typical way people do their CPF nomination by naming their spouse as 100% beneficiary. If both parents unexpectedly pass away, the CPF Nomination will be revoked because the sole nominee is dead. As such, the CPF funds will be distributed according to Intestacy Laws, which will incur admin fees and take a longer time. With the 99% to 1% allocation in place, the children will receive 100% of the CPF funds as the “99%” nominee has passed on.

Final Thoughts: Securing Your Legacy

Understanding CPF nomination is crucial for effective financial planning and ensuring that your savings are distributed according to your wishes. It’s not just about who gets your money, but about providing peace of mind and financial security to those who matter most to you. Whether it’s supporting your family, a loved one, or a cause close to your heart, CPF nomination play a vital role in shaping your legacy.

Reflect on the broader impact: by making informed CPF nomination, you’re not only securing the financial future of your loved ones but also ensuring that your values and wishes live on. It’s a responsibility that extends beyond mere financial planning—it’s about crafting a meaningful legacy.

So don’t wait until it’s too late.

Take a few moments today to review and complete your CPF nomination. It’s a simple step that can make a significant difference in ensuring your wishes are followed and your loved ones are taken care of. Visit the CPF website or the CPF office to get started on making or updating your nomination.

Take this opportunity to think critically about how your CPF nomination can reflect not only your financial intentions but also the legacy you wish to leave behind. It’s an empowering step that shapes the future for your loved ones.

If you have already nominated your beneficiaries, you should review it every year or two as many things can change within a single year, be it relationships or your finances. Similarly, you should review your financial portfolio regularly with your trusted consultant. If you need any advice, you can reach out to our consultants for a complimentary consultation via the link in the description below: