When choosing a bank for a mortgage loan, you might come across banks offering you an Interest Offset Mortgage Account, designed to help mitigate mortgage interest costs for borrowers with significant idle funds lying around.

So how do these Interest Offset Mortgage Accounts work?

These accounts pay interest rates similar to the mortgage loan package you have taken up, with the earned interest used to offset your loan interest, effectively reducing overall interest payments.

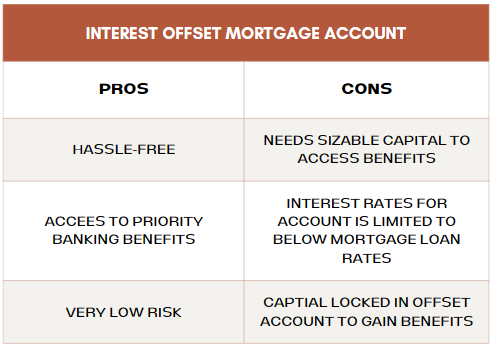

Standard Chartered, Citibank, and HSBC offer such accounts. However, to meaningfully offset the mortgage’s interest requires a substantial lump sum, as there are interest caps imposed by the banks (your interest offset mortgage account funds will earn 50%-70% of the interest rates, of your mortgage loan). Effectively, you have to take a loan with the bank, and at the same time, leave a substantial amount of money with the bank.

While reducing your mortgage interest via an Interest Offset Mortgage Account is a good thing, are there better alternatives?

Current offset accounts require a lump sum and come with interest rates lower than mortgage rates. As of May 2024, the lowest fixed rate for a million-dollar loan is approximately 2.90%, while floating rates hover around 4%. Consequently, offset accounts can only yield up to 2.03% for fixed packages and about 2.8% for floating packages—which is lower than rates offered by fixed deposits!

Knowing this, can we create something better on our own?

Assuming that we have a loan of $1,000,000, and we have about $400,000 lump sum that we can use to offset the interest, let us take a look at two different options that we can use to create our own DIY offset accounts.

For illustration, we will use a mortgage interest offset account that pays 70% of the interest rate of your mortgage loan. As of May 2024, the best mortgage package for $1 Million dollars is 2.9%, meaning the offset account will give us about 2.03% interest rate.

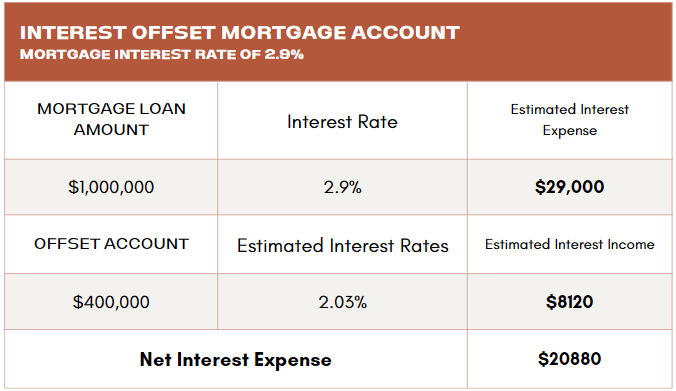

Interest Offset Mortgage Account:

From here, the Offset Account can offset $8,120 in year one. We will use that as our benchmark.

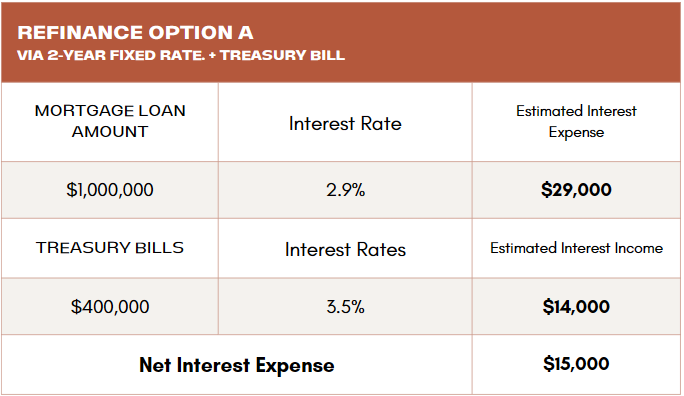

Option A – Using Singapore Treasure Bills

As of May 2024, the most recent SG T-Bills was 3.74%, with previous bills reaching about 3.5%. In this case, we will take a more conservative estimate and use 3.5% instead.

Investing $400,000 in Treasury Bills at a conservative estimate of 3.5% can offset a significant $14,000 of interest in the first year, surpassing the $8,120 offered by interest offset mortgage accounts!

But what if we take a little bit more risk?

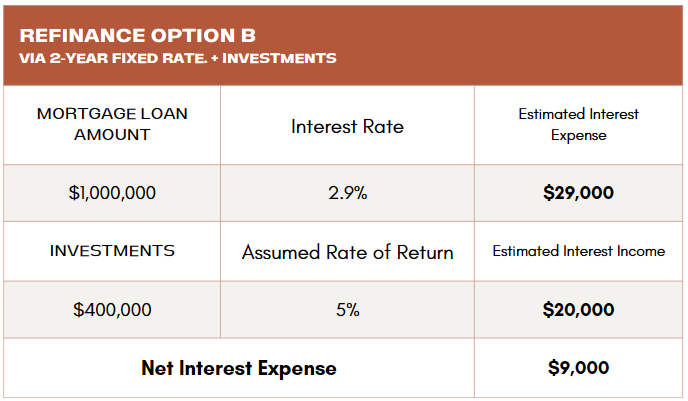

Option B – Investments via Dividends

There are a variety of investments that we can use, but for this case we shall use dividend funds. Dividend funds are designed to payout dividends to their shareholders regularly which is what we are looking for in this scenario, and many of these funds are able to provide an average of 5% per annum.

With a 5% annual return, the dividend funds can help offset a whopping $20,000 of interest in year one! This is a massive difference from what the interest offset mortgage account can offer.

While Interest Offset Mortgage Accounts on paper sound like an attractive feature, it is ultimately limited by the mortgage loan’s interest rate.

Of course, by setting up an account, you may even be eligible to be the priority banking customer for the bank. However, you may be missing out on saving thousands of dollars if you become blinded by the rewards of being a priority banking customer. If you want to take up a new loan, or are looking to refinance, it is always a good idea to consult a mortgage expert on all available options before deciding.

In fact, you can reach our mortgage experts for a free consultation on your mortgage loan, via the link below: