After multiple viewings, you finally decided on the property to purchase and proceed to make an offer. Happily, you contacted your mortgage broker to get recommendations for the best home loan. Next moment, you receive a piece of bad news from your mortgage broker – the amount of loan you can qualify is much lower than what you are expecting.

So, what went wrong?

Before making the offer, you did some checks online and gathered that the current best home loan interest is around 3%. Hence, you did your own calculations based on these lowest market rates and are confident to get enough loan to fund your property purchase.

However, in reality, when calculating the amount of loan you can borrow, the bank does not use the current market interest. Instead, the bank assumes a more prudent Medium Term Interest Rate, which is supposed to be a more realistic indication of the average interest over the period of the loan.

The bank takes the cue from the Medium Term Interest Rate Floor that is set by MAS, which is currently at 4.0%. Most banks peg their Medium Term Interest Rate at a level that is higher than the MAS Medium Term Interest Rate Floor.

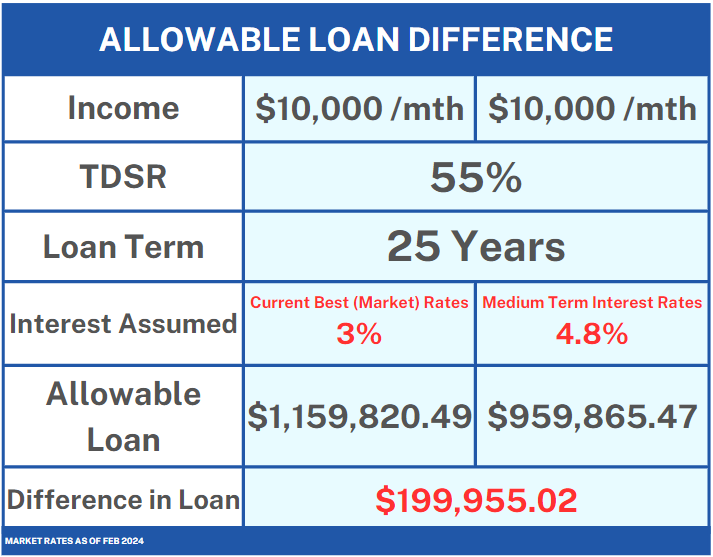

A few banks are assuming 4.8% for the Medium Term Interest Rate currently in Feb 2024. We will examine the difference this makes to the loan quantum you can qualify with an example.

Before that, we need to talk about another concept – the Total Debt Servicing Ratio (TDSR), which is applicable for private properties. This Ratio is the percentage of the borrower’s income that can be used to service all his debts. Introduced on 29 June 2013, this ratio effectively limits the amount of debt an individual can take on. As of Feb 2024, TDSR is at 55%. This means that a borrower can use up to 55% of his income to service his mortgage loan, if he has no other loans.

With a cap on the amount of your monthly income that can be used to service your loan, and the higher interest assumption to be used for loan computation, you will end up with a lower loan quantum.

The common mistake that many buyers make is that they calculate the amount of loan they can qualify by using the (current) Market Interest Rate, which is usually much lower than the Medium Term Interest Rate banks assume.

To give you a glimpse of how big the difference can be, let’s take a look at rates applicable for February 2024. For February 2024, the lowest (fixed rate) loan package is around 3%, while the Medium Term Interest Rate assumed by one of the local banks is 4.8%.

The difference of 1.80% may seem small, but it can translate into a difference of hundreds of thousands of dollars in loan eligibility to the borrower.

Below is an example to highlight the difference. We assume the Medium Term Interest rate is at 4.8%, and the current market rate is at 3%.

As can be seen from the table, the difference in allowable loan is around $200,000. For the uninformed buyers, they might end up having to forfeit the 1% Option Fee paid for the Option To Purchase (OTP), if they fail to qualify for the higher loan amount (based on their assumption using the lower market interest), which will be a costly mistake.

The Medium Term Interest Rate is one of the frequently overlooked points by homeowners, apart from many other factors involved in refinancing. As such, we always recommend you consult an expert when it comes to home loan financing. You can connect with one of our mortgage experts who can help you do a complimentary assessment of your situation via the links below: