Many of our clients are priority banking customers and very often, they assume they are able to get the best home loan package because of their priority banking relationship, but is that true?

Today, we look into a case where we helped a priority banking customer save more than $8000 in interest over two years. Here is what happened:

In March 2023, our client had just secured an Option To Purchase (OTP) for a property and needed a home loan of 4.2 million to finance the purchase. Seeking to get good rates for his home loan, our client went to Bank A, where he is a priority banking customer, for his home loan.

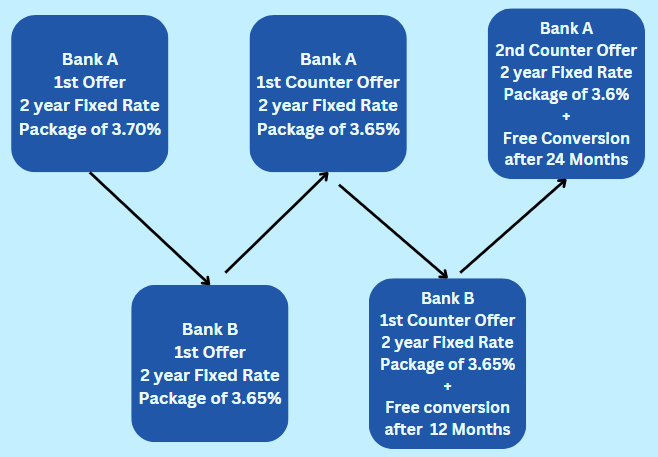

Bank A offered him a 2-year fixed rate package, with an interest rate of 3.70% for the first 2 years. With the average Fixed rate packages hovering around 3.85% – 3.90% at that point in time, it seemed like a good offer. But as a savvy customer, he decided to check in with us to see if we could source for a better deal.

After comparing the packages across all banks in Singapore, we shortlisted 3 banks with the most competitive fixed-rate packages. Floating rate packages were much higher than fixed-rate packages and hence were not being considered. After speaking to the mortgage bankers from these 3 banks, we decided to work with Bank B, who showed strong interest and confidence in securing this deal, and offered a 2-year fixed rate package of 3.65%.

Usually, this is where most cases would have ended. The client found a better package of 3.65% fixed rate, and would have gone with Bank B.

However, because of the high loan quantum involved, we expected to have some counter-offers from the banks involved. This series of counter-offers lengthened the time taken to reach a conclusion. In the end, after 2-3 weeks, the final offer for both banks arrived at the end of first week of April.

The Final Offer:

Bank A:

2-Year Fixed Rate Package: 3.6% + Free Conversion to any Package within Bank A After 24 months

Bank B:

2-Year Fixed Rate Package: 3.65% + Free Conversion to Any Package within Bank B After 12 months

This is where the features offered become very interesting. A Free Conversion feature is very common in the industry, but is often available only after the lock-in period. In this case, it should have been after 24 months.

However, Bank B broke convention and offered the client a Free Conversion after only 12 months, which is within the lock in period! In fact, we believe this is the first time this feature (free conversion after 12 months) was made available in a home loan package.

With this free conversion after 12 months, the client can freely change to any other package within Bank B after the first year even though his loan is still within lock-in period.

So, if the market interest rate were to drop in a year’s time, the client is free to switch to another package with lower rates.

On the contrary, if the market interest rate were to rise, he can continue with the fixed year 2 rate of 3.65%. In short – “Head or Tail – the client wins!

As a result, the client opted to go with our recommended Bank B’s offer, and rejected the lower interest package from his priority bank A.

While Priority Banking can indeed get you the best package within that bank, it may not necessarily be the lowest rate or the most suitable package. A Mortgage Broker can help you negotiate between banks, especially if your loan quantum is substantial.

Compared to the best market interest (fixed rate) of 3.75%, we managed to help our client secure a lower offer of 3.65% interest rate, with an additional unique feature – Free Conversion after 12 Months.

The “0.1%” lowering in interest would have saved him at least $8,000 in interest over 2 years! And if interest were to fall after 12 months, the actual savings would be way more than just $8000, by converting to another lower interest package within Bank B.

Do you need a new loan, or is your current loan out of the lock-in period? Get in touch with our mortgage specialist for a free consultation on the best package available for your home loan. You can reach us via the link below: