As at 08 December 2023, there are still 57,000 home owners with SIBOR-pegged home loans who have not switched out to alternative loan packages. After 31 December 2024, SIBOR, or Singapore Interbank Offered Rate, will be replaced by SORA, Singapore Overnight Rate Average, and all remaining borrowers will be forced to convert to SORA-pegged loans.

All banks stopped issuing SIBOR-pegged loans after September 2021, which means most of these SIBOR loans are out of “lock-in”, and the borrowers are free to refinance to another bank. Back in 2021, where mortgage loan interest was as low as 1%, borrowers were not as “hard-pressed” to quickly switch their loans out.

But currently, SIBOR has risen to 4.05%. With a typical loan spread of 0.75% -1%, the effective interest that these SIBOR loan borrowers are paying currently will be around 4.80%-5.05%.

Many homeowners are caught off guard by the huge surge in interest rate, which rose in tandem with the 11 rounds of interest rate hikes since March 2022 by the Federal Reserve. Let’s take a look at the impact of this surge in interest on a typical private home loan:

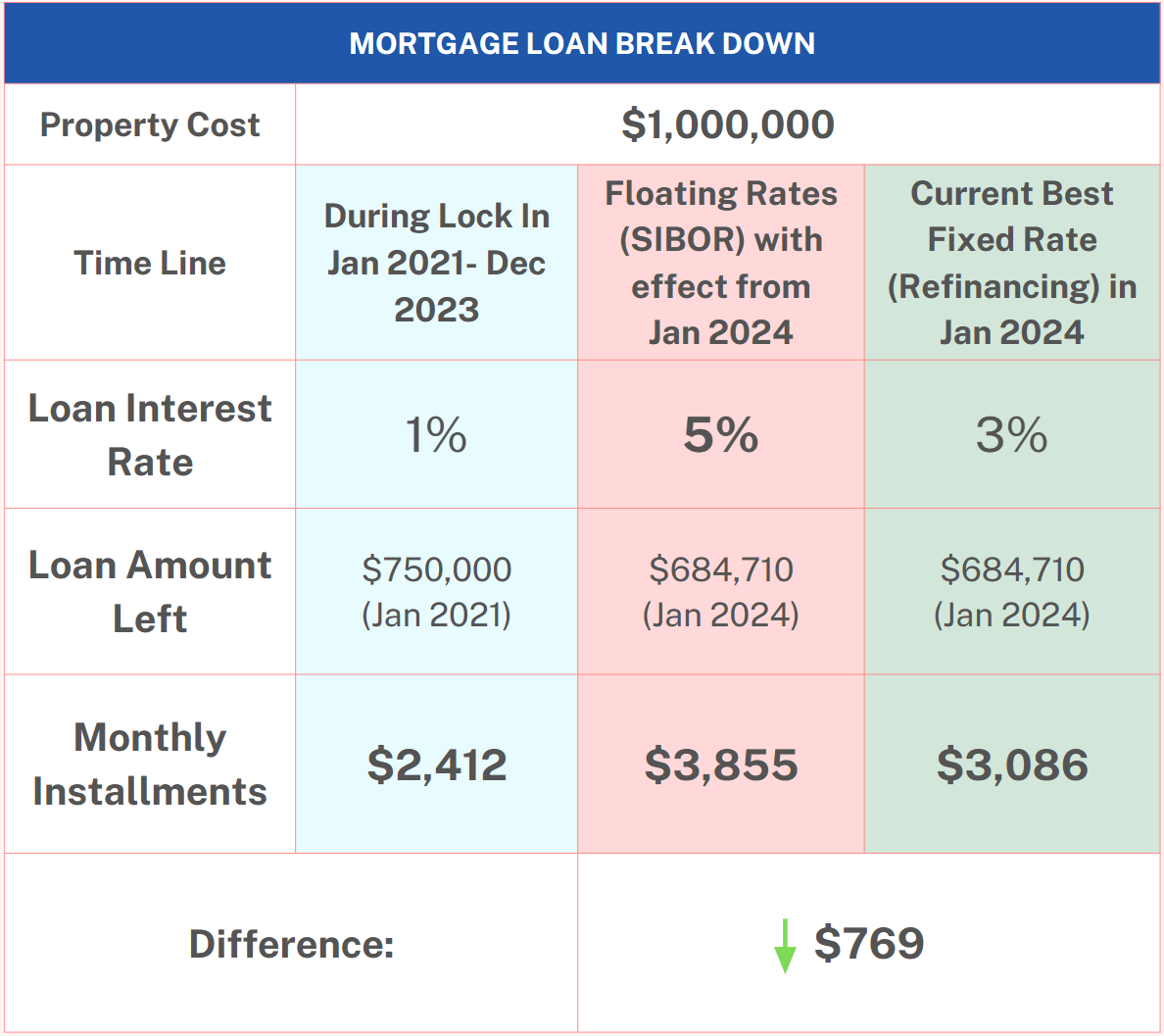

Assuming a property value of $1 million and the owner borrowed $750,000 in January 2021, and took up a 3 year fixed rate of 1% interest rate (for 1st 3 years), and loan tenure of 30 years. The monthly installment would have been $2412 for the first 36 months. Now, in Jan 2024, the interest will be on floating basis (SIBOR) after the fixed rate ends, with an effective rate of 5%. Meaning, their monthly installment is now $3,855.

Previously they were paying $2,412 for their monthly installments, but at the current interest of close to 5%, the monthly installment is now $3,855. That is a 59% increase in monthly payments, or additional $1443 per month.

So, what can this homeowner do?

As of Jan 2024, the best fixed rate packages are hovering around around 3%. If this borrower were to refinance to a 3% loan, he would be able to reduce his monthly payments to $3,086. Saving them close to $800 per month in terms of monthly installments alone. However, the saving in interest is actually $13,644 and $27,166 over the next 1 year and 2 years respectively.

That is – $27,166 saved by doing a simple refinancing.

*Assuming the 2nd year rate is still 5% after forced conversion to SORA rates.

With inflation hitting record high on all fronts, many Singaporeans are feeling the heat. Like what we always say – the banks are rich enough – you don’t have to contribute more to their annual profits!

![]() If you are a homeowner who is paying an interest of more than 3% in 2024, you are definitely overpaying. For a free assessment of whether you are eligible to save some money on your home loan interest, you can consult one of our home loan experts via the links below:

If you are a homeowner who is paying an interest of more than 3% in 2024, you are definitely overpaying. For a free assessment of whether you are eligible to save some money on your home loan interest, you can consult one of our home loan experts via the links below:

Whatsapp – The Financial Network

Contact us – The Financial Network

12th Jan 2024