When taking up a home loan or mortgage, you may be presented with two different types of packages, Fixed rate packages and Floating rate packages. These two terms would be very familiar to seasoned property owners as they often have to revisit their mortgage broker every 2 or 3 years to refinance and lower their interest.

So, what are the differences between these two types of loan and which one should you go for?

What are Fixed Rate Packages?

These loan packages offer you a fixed interest rate for 2 or 3 years where the interest rates are fixed for the initial 2 or 3 years (also known as the lock-in period). After the lock-in period, the loan would then switch to floating rates, where the effective interest is usually pegged to 3-month Compounded Singapore Overnight Rate Average (SORA) rate, plus a loan spread (the lender bank’s margin). Under normal circumstances, fixed rate package interest will be higher than the effective interest of a floating rate package, to compensate the bank for taking a risk by guaranteeing your interest rate for 2 or 3 years.

When do we pick Fixed Rate Packages?

Fixed interest rate offers you peace of mind knowing that your loan’s interest rate would not change, and your monthly installment amount is the same month after month. But it also means that if market interest drops, you are locked into paying a higher interest (and installment) during this period.

So, the best time to get a fixed rate is when market interest rates are rising, and you want to lock in the lower interest rates (now) so that you would not be paying higher and higher interest over the next 2 – 3 years.

What are Floating Rate Packages?

These loan packages are subjected to periodic adjustments depending on the “reference rate” that it is pegged to. The reference rate could be the bank’s internal board rate (such as Fixed Deposit) or more commonly, the 1-month or 3-month Compounded SORA. If your loan is pegged to the 3-month SORA, your Effective Interest Rate will be adjusted every 3 months. Consequently, your monthly installment will change every 3 months. The bank adds a loan spread to the reference rate, and together it will give you the Effective Interest Rate you will be paying. During times of market volatility, the month to month Effective Interest can vary significantly, and hence affects your monthly installment.

When do we pick Floating Rate Packages.

These packages are ideal when market interest rates are falling and you would then enjoy the successive lowering of interest rates (and monthly installment) along the way after taking up the package.This can happen when you take up your package during times of “peaked market interest” where the rates are likely to trend downwards subsequently.

In short, when markets are going up, pick Fixed Rate Packages. When market interests are going down, pick Floating Rate Packages.

As an example:

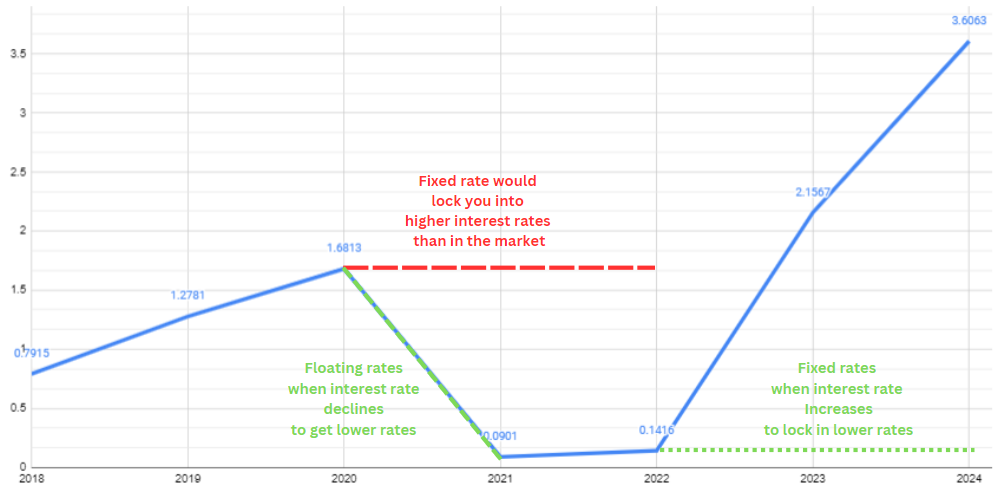

In 2020, when the COVID-19 Pandemic hit, we saw market conditions slow down and interest rates falling to historic lows. At that time, when interest rates are falling, it would be a good time to go for Floating Rate Packages, as SORA rates were falling to as low as below 1%

However, as the economy recovered, it began to rise again in 2022, with SORA rising from sub 1% to 2.9%. During this period, it would make a lot of sense to pick a Fixed Rate Package, so you can lock in the current low interest rate for a few more years.

While in hindsight, it may be easy to say which is the better choice, it is much more difficult to make a decision in the present. Admittedly, no one can accurately predict the future but industry professionals are still able to gauge the general direction of the market, barring exceptional circumstances like another global event or trade disruptions.

Also, historically, Fixed Rates are often slightly higher than Floating Rates. This is because you are paying for the security of the Fixed Rate. But these few years, we are in unusual times where the Floating Rates are higher than Fixed Rates, making it even more complex.

As such, it is always recommended you consult an industry expert regarding your home loan. For that, you can get in touch with our mortgage experts for a free consultation, and also get access to the lowest loans across all banks in the country via the link below: