So your Loan is out of the lock-in period and the interest rate you are paying on your loan is now at an all-time high. Should you Reprice your loan, or Refinance it? Let us take a look at both options.

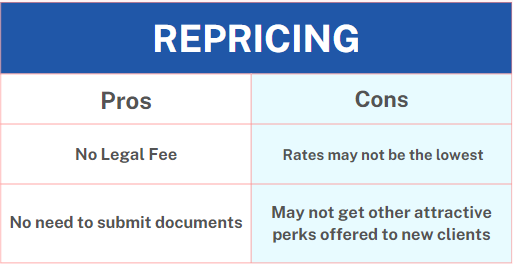

Repricing

is when you re-negotiate new terms for your existing loan with the same bank, often to try and lock in lower rates for the next few years. Here are the pros and cons:

Pros:

- No Legal Fee – There is no legal fee involved since the loan remains with the same bank. However, some banks charge an Admin Fee for Repricing.

- No need to submit documents – you do not need to go through the same rigorous loan application process and credit assessment (when you first took up the loan)

Cons:

- Rates may not be the lowest – Existing clients may not receive the lowest interest rates, as banks often offer better rates to attract new clients due to competitive pressures. As such, the rates you get within the bank would often not be the best in the market.

- Existing clients might miss out on additional perks available to new clients – For example, a homeowner planning to sell within the next 12 months may benefit from a package that includes a Waiver of Penalty for full loan redemption during the lock-in period.

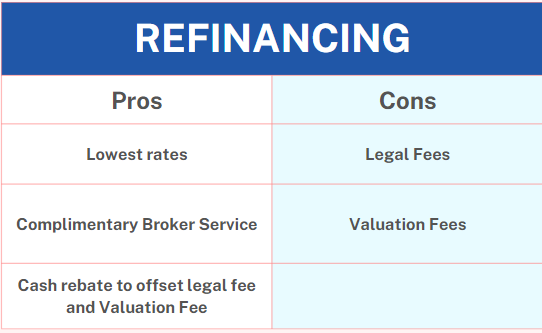

Refinancing

is when you replace your existing loan (from Bank A) with another (from Bank B). Here are the pros and cons:

Cons:

- Legal Fees – There will be legal fees involved for switching from one bank to another, and typically the cost is between $2000-$2500

- Valuation Fees – you will incur a valuation fee of between $200-$500.

Pros:

- Lowest rates – Different banks take turn to offer the most competitive rate packages. By comparing packages across all banks, you can secure the most attractive deal, potentially saving tens of thousands of dollars when refinancing a private property.

- Complimentary Broker Service – the services provided by a loan broker is typically free. And he will be able to help you compare across 12 to 14 banks and financial institutions in Singapore. An experienced broker will also be able to guide you through the refinancing process and make it as hassle-free as possible

- Cash rebate to offset Legal Fees and Valuation Fees – most banks do provide cash rebates based on the loan quantum. With this, you will be able to cover almost the full amount of your legal and valuation fees.

Ideally, you should ask your existing financier to quote you for the Repricing package. Concurrently, you should get in touch with a mortgage broker to compare the rates from the different banks. You can get in touch with our mortgage experts for a free consultation on how to get the best deal for your mortgage loan via the link below